Efficient Wealth Update -January 2021

The War on Investment Management: Active versus Passive

COVID-19 has, undoubtedly, thrown the world into universal, explosive unrest. Across the globe we have witnessed numerous protests and riots against economic hardship, police brutality and political instability, most acutely exemplified by the recent ‘storming’ of Capitol Hill in America, which some believe is a precursor for civil war. But whether you subscribe to this view or not, there is one war that has been waging for many years that many of us have overlooked: the war on investment management.

There are two clear schools of thought when it comes to how your investments should be managed: active and passive. But, as an investor, why should understanding these concepts be a key concern?

What Is the Difference?

As investors, you generally will have two main investment strategies that can be used to generate a return on your investment accounts: active portfolio management and passive portfolio management.

Active portfolio management focuses on outperforming the market in comparison to a specific benchmark, whereas passive portfolio management mimics the investment holdings of a particular index in order to achieve similar results.

As the names imply, active portfolio management usually requires more frequent trades and involves guidance from an Investment Manager, whereas passive management does not have a management team making investment decisions and the trade frequency is determined by the investor directly. In addition, active management strives for superior returns, but generally takes greater risks and entails larger fees than its passive counterpart.

COVID Performance

The chart above shows the relative performance of the seven points on the risk spectrum we track versus that of just the pure asset allocation (i.e. no active management). Whilst early on in the pandemic portfolios underperformed relative to the market as a whole, as the recovery pushed ahead, all portfolios ended delivering a positive return relative to passive, net of costs, by the end of the year.

To give an explanation of what happened, at the start of the pandemic all assets fell as the markets were swept up in a panic of selling. Lower risk profiles, with more exposure to credit and corporate debt suffered initially, but recovered well thanks to Quantitative Easing.

Medium to Higher Risk Profiles have more equity content (shares). At the start of the pandemic, the active selections in these funds underperformed compared to their passive alternative; however, smaller companies began to make a steady recovery over the year as we learnt to live with the pandemic. Then towards the end of the year, with the news of a vaccine on the horizon, caused value investments to perform well. Value companies are ones that have fallen out of favour and are priced lower than their peers, therefore sectors that were hit hardest by the pandemic started to see light at the end of the tunnel.

What Does This All Mean?

- The active return on an investment (Alpha) can often be erratic and doesn’t perform on demand.

- Just because we pay for extra performance doesn’t guarantee it will outperform its passive alternative; however, over time we should hopefully see the results if we can suffer some underperformance in the short term.

- It’s important to stay diversified. As an example, PortfolioMetrix (one of our Investment Managers) ensure their portfolios are well diversified across large and small companies, value vs growth/quality, currency exposure, asset classes and geographical location.

- If we believe in a particular fund or investments strategy, we shouldn’t give up on it due to a period of underperformance, quite the opposite. PortfolioMetrix rebalanced back into the hardest hit funds in March and that added to performance over the year.

- Passive has its place and if you want to reduce costs it’s a sure-fire way to go, but if we can deliver extra returns net of costs over time then that could be a worthwhile endeavour.

Understanding the best investment strategy for your needs can often be confusing, so we encourage you to speak to your Financial Planner at Efficient Portfolio if you have any concerns with performance, management type or risk associated with your portfolio.

Please get in touch on [email protected] or call 01572 898060 if you have any concerns.

How Can You Best Save for Retirement?

Saving enough for retirement is a huge financial hurdle that you need to be able to get over to be able to live out a comfortable and secure future. As a firm, the one question we are asked time and time again is ‘How can you best save for retirement?’ It’s a great question, however there is so much more to saving than knowing just how much enough is. The place to start is to firstly ask yourself a number of key questions:

-

How Much Should I Save for Retirement?

The answer is it depends on how old you are. The simplest method of calculation, which is a useful tool for those people in their twenties and possibly their thirties, is to save ½ your age as a percentage of your earnings. So if you are 24, saving 12% of your earnings for your retirement is a good guide.

This is a good starting point, but the closer you get to retirement, the more scientific you need to be. This is where a Lifetime Cash-Flow Forecast can give you much greater clarify, as you can take account of your actual spending habits, growth rates of your investments and time in retirement.

-

What Investments Should I Pick for My Pension?

The further you are from retirement, the more risk you can afford to take. You are likely to have a rockier road to retirement the more risk you take, but in the long run, you are likely to end up with more. That said, if you take too much risk, you might end up with nothing, so it is a fine balance.

Select an investment strategy that gives you a good asset allocation, i.e. a good spread of investments, such as equities, bonds, property and commodities. The blend of these should be determined by the level of risk you are willing to take, but needs to be balanced in line with the ‘Modern Portfolio Theory’ to ensure you get the best returns possible for a level of risk you are comfortable with.

-

When Should I Start Saving for Retirement?

Ideally yesterday! Seriously though, if you look at a standard piece of paper (0.05mm thick) and folded it in half 50 times, it would reach about 100 million kilometres high, which is about two-thirds of the distance between the Sun and Earth. Amazing, isn’t it? That is compound growth at work. The sooner you start the further you will get.

-

How does this help your pension?

The longer you can leave your money to grow, i.e. the sooner you can start, the more impact doing so will have on your savings, because you will benefit from growth on the growth. Let’s look at an example:

Mr. Jones is 40 years old and he decides he is going to save £100 per month until he retires at age 65. He invests in a fund that grows at 6% each year. Over that 25 years, he has invested £30,000, but with the growth on the growth on the growth, his fund would actually be worth £107,000. That’s growth of 360% over the 25 years—not bad.

What if Amy Jones, his daughter, also decides to start a pension at the same time? She is 20 years old, and can only afford £56 per month into the same 6% fund. Coincidentally, this means she also invests £30,000 between 20 and 65. So she has put in exactly the same amount of money as her Dad, but over 45 years instead of 25. Instead of the £107,000 that Mr. Jones’ pension reaches, Amy’s pension will be worth £153,000. That is 510% growth instead of 360%. To look at it another way, that’s 43% more than her Dad had for saving the same amount, because her money is invested over a longer period of time. The sooner you can start saving, the better it will be. Even if your monthly savings don’t seem like large amounts, over time the money will grow.

-

Is a Pension the Best Place to Save for Retirement?

Quite simply, yes. It is currently the most tax efficient place to save to generate an income for later in your life. Effectively you are deferring tax today to pay less later on, whilst benefiting from tax free growth in the meantime.

So if you aren’t already saving for your retirement, get started now- this is how you can best save for retirement. If you are saving, but it isn’t enough, take action now. If you don’t know where the money is invested, make it your week goal to find out. Take a huge stride towards your dream retirement.

Is Now the Time to Review Your Protection Portfolio?

The pandemic has changed the way we work forever and forced many of us to reconsider how we work, where we work and who we work for. However, if this sounds like you, are you confident that you have considered what you could stand to lose? And are your certain that your standard of living, and the security of your family, won’t be negatively impacted?

One upshot of the last year is that many people’s view on their working life has changed. Whilst this might have been forced on some through redundancy or an extended period of time on furlough, others working from home might now have reflected that the daily grind of commuting into a dreary office is no longer for them, and as the market recovers they are considering a change in their role, going part-time, or even switching career to protect the newly found ‘me-time’. The more entrepreneurial might even have found time in lockdown to set up their own business, which they hope will flourish once we’re all allowed out again.

At times like this it’s important to consider the benefits that are provided by your employer that you might have lost. Often employers offer death in service benefit, which is valuable for both covering debts and providing a nest-egg for loved ones if you’re no longer around. However, the benefit is usually linked to your salary, so if it’s reduced the level of cover will fall accordingly. In addition, some larger employers might offer higher levels of sick pay, which again will shrink if your working hours fall, or disappear completely if you leave to set up on your own. Another consideration you need to bear in mind if you’re thinking of leaving your current role is pension contributions, which all employers now provide at least 3% of your salary towards- if you leave, or take a salary reduction, these contributions will fall or be lost all together.

Whilst it is important to weigh up the pros and cons of changing your working arrangement, especially if you are considering becoming self-employed, the loss of benefits does not necessarily need to be a reason to stay put.

Ultimately, all these benefits can be replicated privately, through Life Assurance Polices, Income Protection Plans and Personal Pensions, so there are plenty of options available to make sure you and your loved ones remain protected both now and in the future.

Protection is a cornerstone of financial planning for many people, so whether you are considering making a significant change to your employment, or if your situation has recently changed, we strongly encourage you to review your cover before making any final decisions. Protection can act as your ‘safety net’ for the future, so now is the opportune moment to ensure that there aren’t any gaps or snags in your current arrangements.

If you would like to look at your options, we would be delighted to help. Please email [email protected] or call 01572 898060 to speak with one of our Independent Financial Planners.

LPAs Go Online

In the August 2020 Wealth Management Update we mentioned the possibility that the administration of LPAs would move online and it seems all the hard work by the Office of the Public Guardian (OPG) (likely urged forward by the need to be more online during the pandemic) has paid off!

The OPG has been working closely with a range of organisations, including HSBC UK and the Department for Work and Pensions (DWP), to develop the service and has announced the ‘Use a Lasting Power of Attorney’ service. This allows donors and attorneys to give organisations access to view an online summary of an LPA.

Once an LPA is registered, attorneys and donors will be sent an activation key. They can create an account online at https://www.gov.uk/use-lasting-power-of-attorney and use the activation key to add LPAs to their account. A donor or attorney can then create an access code which they can give to organisations.

Anyone who has had to register an LPA with an institution will know how long it takes to get through to the right department, to send in the original LPA, to wait for it to be loaded on to their system and for them to process it, then to wait for the original LPA to be returned to you before you can tackle the next institution, all the time not being able to access or manage the donor’s assets … it is making me tired just thinking about it.

These long turnaround times should hopefully be reduced to days using the online service, resulting in the Lasting Power of Attorney being registered much faster and without having to rely on original documents making it safely to their destination.

I hope institutions will see this as a leap forward in the use of LPAs and a vast improvement on any existing system. With luck they will all adopt the new system and start using it immediately to make donor and attorney lives easier.

Currently you can only use this service for LPAs registered in England and Wales on or after 17 July 2020. However, as we mentioned last year, this is likely to be extended to those registered in previous years … watch this space.

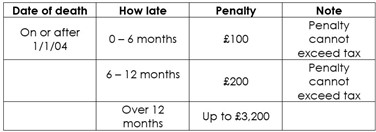

Inheritance Tax – Chargeable Penalties

Now more than ever it is important to be on the ball with any outstanding inheritance tax. HMRC have imposed an initial deadline of 12 months from the date of death for you to submit the relevant inheritance tax account. In the current climate it is important to factor in additional delays caused not only by the postal system and institutions but also potential delays within HMRC itself.

If you submit the inheritance tax account 12 months or more after the initial 12-month deadline, the fine can increase from the standard £100–£200 late filing penalty to up to

£3,200 in total. The main penalties that you may need to be aware of are:

Please contact your adviser if you want to ensure that you avoid incurring any unnecessary late fees.

House Prices See Highest Growth in Six Years

House prices rose by 7.5% throughout 2020 – surprising in the current circumstances but welcome news for homeowners.

The furlough and self-employment income schemes provided vital support to the market and the cost of borrowing remained low because of a whole host of factors and so kept available credit flowing. Coupled with the fact that lenders were able to offer payment holidays to borrowers to help them remain in their homes meant that the property market ended 2020 on a high.

Without doubt, the stamp duty holiday has also been a stimulus to the market, as lenders approved more than 100,000 mortgages in November – the most in 13 years! However, it has also been helped by the public’s desire to have more space for their families, both inside and out, as the pandemic has restricted people to their homes for most of 2020 and potentially a chunk of 2021.

Competitive mortgage rates are still available and lenders are starting to allow smaller deposits again, having increased the minimum required during the height of the pandemic. However, both lenders and conveyancers are struggling to keep up with demand and all currently have a backlog of requests. This means that some buyers may potentially miss out on the stamp duty holiday they were hoping to get.

Whilst the outlook for 2021 remains uncertain, especially after the end of the stamp duty holiday on 31st March, hopefully as the vaccine continues to be rolled out there will be increasing stability across all markets.

NS&I Complaints

As a result of poor service levels from NS&I in recent months MPs have ordered NS&I to investigate because of the anxiety caused to many of its customers.

When NS&I recently slashed the chances of winning on Premium Bonds and dramatically cut interest rates across all products, consumers were eager to move their funds to higher paying providers. However, when customers attempted to withdraw their funds, they were met with long delays and reduced service, in part because of the pandemic but also because of poor management that was already evident before the pandemic struck.

NS&I have recruited almost 200 additional customer service staff to try to improve their call capacity and overall service levels and hopefully this will help with future interactions. However, those who suffered difficulties during a time when their interest rates were drastically reduced may not be quick to forget their experience.

Please note: NS&I have decided to stop paying Premium Bond winners via cheque as of Spring 2021. Winnings will be paid directly into bank accounts in the future.

Do Not Forget Self-assessment!

The deadline for submitting your 2019/20 self-assessment tax return is midnight on 31 January 2021.

Those who are late submitting their return face a penalty of £100, even if there is no tax to pay or if tax owed is paid on time. Additional penalties are due for continued late filing and late payments.

Charlie’s Mini Blog

Yesterday I was watching a brilliant presentation by Mark Robb on driving employee engagement. A couple of things he said really struck a chord with me. The first was that your team need to be constantly growing, something the team at Efficient Portfolio certainly understand, as part the ‘P’ of the The EP Code (our company culture) stands for ‘Pursue Growth and Learning’. Mark’s point is that if any employee is not getting better and better each year, they are actually going backwards, because everyone else should be improving.

The same could be said for our money and many other aspects of our life. If we leave our money in the bank, whilst it stays the same value, everything else is gradually getting more expensive, so what you can buy with it is going down. If we don’t try and gradually improve our health and fitness, it will inevitably go backwards due to aging. So pursue growth and learning in everything you do.

The second point that really struck home was, to steal his words, ‘don’t try and teach a pig to sing!’ To put it another way, you wouldn’t send Lionel Messi for goalkeeping lessons, far better for him to focus solely on his strengths. We try and apply this approach to our team, trying to all work to our own unique abilities, but do you do the same in your life? Do you get bogged down doing something that isn’t your unique ability, when you could be spending your time doing the activity or role that is, delegating that task to someone else who’s unique ability it might be. If you don’t, you may be just trying to make a pig sing!

Book Recommendation

‘Peak Performance: Elevate Your Game, Avoid Burnout, and Thrive with the New Science of Success’ by Brad Stulberg and Steve Magness was one of the best books I read in 2020. It combines the inspiring stories of top performers across a range of capabilities from athletic to intellectual to artistic with the latest scientific insights into the cognitive and neurochemical factors that drive performance in all domains.

It looks at the common traits amongst the most successful people across various disciplines including Olympic marathoner Meb Keflezighi, three-time Grammy Award winner Don Was, and renowned mathematician David Goss and gives you strategies so that you can copy them.

Unlike other performance books that are field-specific, Peak Performance cuts across domains and will help people involved in diverse pursuits, from athletes to artists, from hobbyists to scientists, from students to business professionals. If you want to take your game to the next level, whatever 'your game' may be, Peak Performance will teach you how.