Efficient Wealth Update – March 2020

Market Update

Markets sold off sharply on Monday, on the back of a fall in the oil price of well over 20%. Saudi Arabia had been attempting to organise production cuts to support the oil price after COVID-19 impacted demand, but Russia failed to back the plan leading to Saudi Arabia threatening to raise production next month and offer its crude oil at a deep discount. The FTSE 100 was down around 7.7%, a significant portion of this driven by index heavyweights BP and Royal Dutch Shell which are down between 15% and 20%. The S&P 500 was down almost 6%.

It is at times like these that we see the importance of investing in a diversified portfolio. The chart below shows the losses received on portfolios ranging from 1/100 on the risk scale (low risk) through to 100/100 (high risk). As you can see, even the highest risk portfolios have fallen significantly less than the markets.

The oil price fall was a serious shock to the market, as is evident by its dramatic spill-over into equity and bond markets. It is, of course, also linked to the ongoing effects of the coronavirus, both in the sense that COVID-19 caused the initial oil price weakness that flared into Saudi Arabia/Russia disagreement but also in the sense that falls have been magnified by general coronavirus uncertainty in markets.

The oil market has bounced back a bit, from a low of under $32 per barrel to almost $37, but clearly the energy industry is under pressure, as are most cyclical sectors exposed to global growth that is likely to be challenged this year.

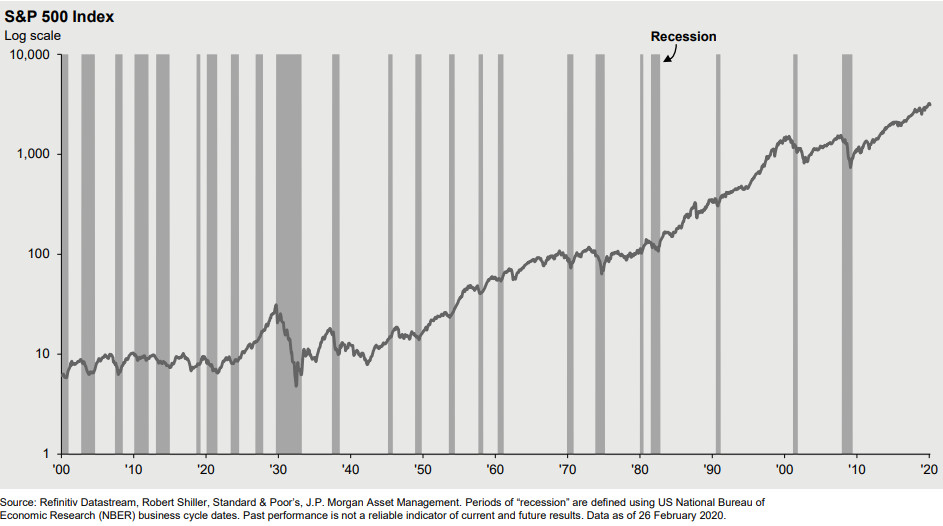

Market falls, and the falls in portfolio values they cause, are always unpleasant to experience. Diversification can help mitigate the magnitude of these falls (and is doing so currently) but clearly cannot eliminate the falls completely. After all, volatility is the ‘cost’ of achieving above inflation returns over the longer-term. Composure is definitely tested in extreme markets. Some clients deal with challenges to composure by not focusing closely on the day-to-day fluctuations of their portfolio, but for those that do get stressed by daily/weekly/monthly falls, it can be helpful to take a step backwards to look at the bigger picture, and specifically the performance of equities over multi-year time-horizons more in-line with the typical horizon of a client’s financial plan.

As an example of this, the below looks at the price returns of the S&P 500 over a 120-year period using a log-scale. Over this longer time period, even the falls that occur during a recession (the grey bars), however horrific they feel at the time, don’t look as serious.

Source: J.P. Morgan Asset Management

And please keep in mind that the index above doesn’t include the dividends paid out by the S&P 500 over time. If you did that, the long-term returns would look even better, more than compensation enough for sticking with your investments during difficult times. We are not yet in a recession. Sliding into one isn’t what we expect, but even if we do the PortfolioMetrix portfolios are very well diversified and made up of what we think of as very high-quality funds with solid underlying investments. We believe in them for the long-term.

In fact, rather than seeing times like this as scary, instead consider them a chance to buy into a market at a much lower cost; i.e. getting more value for your money, with more scope for future growth. Thankfully as a result of the work we do educating clients about risk, we have overwhelmingly had more calls from clients wanting to invest more than we have had with worry at their heart.

The secret to getting long term growth is withstanding short term falls!

The Budget 2020

Chancellor Rishi Sunak has delivered his first Budget in the House of Commons, announcing the government's tax and spending plans for the year ahead. There wasn’t a huge amount that relates to personal finance, but here are the key bullet points that are worth being aware of:

The big ones;

- Pensions tax breaks for higher earners are to be made more generous from next month. The income threshold at which tax relief on pension contributions starts to shrink will rise from £110,000 to £200,000. However, at the same time, the minimum floor which the annual allowance could apply to for higher earners will fall from £10,000 to £4,000.

- Entrepreneurs' Relief will be retained, but lifetime allowance will be reduced from £10m to £1m

- The amount families can save into a Junior Isa or child trust fund will more than double in 2020-21, from £4,368 to £9,000 in April.

The rest;

- National Insurance Contributions tax threshold to rise from £8,632 to £9,500 - saving employees just over £100 a year

- 5% VAT on women's sanitary products, known as the tampon tax, to be scrapped

- Business rates in England will be abolished for firms in the retail, leisure and hospitality sectors with a rateable value below £51,000

- Business rate discounts for pubs to rise from £1,000 to £5,000 this year

- VAT on digital publications, including newspapers, books and academic journals to be scrapped from December

- Stamp duty surcharge for foreign buyers of UK properties to be levied at 2% from April 2021

- Statutory sick pay will be made available from the first day of self-isolation, even if no symptoms are present.

Use it or lose it ...

With the end of the tax year a mere month away here is a reminder of the allowances you should not miss out on.

- Personal Allowance - if you aren't earning enough to fulfil your Personal Allowance (currently £12,500) then you could release some money from your investments to use up this allowance and potentially not pay tax on that money.

- CGT Allowance - an opportunity to take investment profits of up to £12,000 (2019/2020) "tax-free" each year - worth £2,400 a year for a higher rate taxpayer.

- ISA Allowance - if you don't use it, you lose it. A total of £20,000 across all of your ISA accounts that could be earning money in a tax-efficient environment.

- Pension Annual Allowance - whilst this can be carried forward for a number of years, you must have the relevant earnings for the contribution in the tax year in which you contribute, so if you have the allowance and the earnings this year it might be best to use it up.

- Gifting - there are a number of gifting allowances that may be beneficial for Inheritance Tax purposes. Have a look on the HMRC website for more info: https://www.gov.uk/inheritance-tax/gifts

- You should seek advice to see if using any of these allowances is suitable in your situation so, if in doubt, get in touch.

Chancellor resigns weeks before budget

We touched briefly on the Budget last month in regard to the tax break for high earners in the NHS. However, what the Budget will look like has been thrown into question following the resignation of Sajid Javid just a few weeks ago.

Javid resigned because of a conflict over a request for him to fire his existing team of advisers in order to remain in his role. Unable to accept these conditions, he was replaced by Rishi Sunak who only seven months ago held the role of Junior Housing Minister.

Despite this turmoil, the Budget is still set to go ahead on 11th March and is expected to bring much reform. The large Conservative majority means that the Chancellor has practically free rein to bring about whatever change he sees fit.

Changes to tax, pensions, housing and social care are all likely to feature, as well as increased spending in the north of England as the Conservatives tip their hats to the voters who helped the party come to power. We will need to wait to see exactly what changes will be implemented and whether the recent Chancellor-swapping has any effect.

Trust registration service delays

You may have heard that HMRC plans to implement the amended trust registration service this year. The effect of this will be that almost all express trusts will have to be registered, rather than only those that have tax liabilities. This is a large administration task and the registration process involves collecting and providing details of the people affected by all trusts, e.g. settlors, trustees and beneficiaries, as well as the trust assets.

The initial consultations indicated that this change would come into place at the start of 2020. Over 200 responses were received to the consultation and these responses need to be properly considered. Therefore, the proposed deadline of March 2020 for implementing the changes to trust registration has been put on hold.

The technical consultation on this matter closed on 21st February 2020 and we are currently waiting for the outcome to be announced. This will hopefully provide more clarity on when the trust administration service changes will come into force and we will be in touch to let you know how this might affect you.

Premium Bonds on balance

NS&I Premium Bonds are the UK's biggest and most popular savings product, with around 22 million people saving more than £85 billion. In a nutshell, Premium Bonds are a savings account where a monthly prize draw determines any interest (prizes!) that is paid. The prizes, which range from £25 to £1 million, are paid tax free and you can access your money whenever you want to.

However, since the launch of the Personal Savings Allowance (PSA) in 2016 this tax-free incentive for savings is no longer seen as such a bonus. However, for those who would pay tax, Premium Bonds still have something to offer as prizes do not count towards the PSA. With Premium Bonds there is also no risk to capital as NS&I is backed by the Treasury and this safety net is often seen as a real advantage.

Some not-so-good news for Premium Bond holders is that from May 2020 the annual prize rate is dropping to 1.3% (from 1.4%), meaning the chance of a £1 bond winning any prize will be lowered to 1 in 26,000, from 1 in 24,500. This is only an 'average' benchmark of the potential returns however, as there is obviously no guarantee you will win anything at all - and of course it's still the case that the more bonds you have the more likely you are to win.

Overall, Premium Bonds can still have a place for "on deposit" savings if they complement your other savings and investments. They are likely to be most advantageous if you are particularly lucky, or if you are a higher or additional rate taxpayer who has used up their Personal Savings Allowance, your ISA allocation and your Capital Gains Tax allowance. They are a good home, for example for relatively short-term savings, like money you’ve put aside for a future tax bill. Of course, you may have better than average luck, but don't bank too hard on winning the jackpot ...

New £20 for 2020!

Following the success of the new polymer £5 and £10 notes, the Bank of England fittingly launched the new £20 note on 20th February. Equipped with new security considerations, the plastic cash is harder to replicate, making it difficult to counterfeit. A hologram image with the words "Twenty" and "Pounds" along with see-through windows with metallic pictures in blue and gold foil make forging more difficult for fraudsters. There is currently no set date for the withdrawal of the old paper £20 notes so you can continue to spend your paper notes as usual and six months' notice will be given once the final withdrawal date is agreed. For collectors out there, keep an eye out for any low or sequential serial numbers such as 123456 or 333333 on the new notes.

Charlie’s Mini Blog

Last week I was at the Science of Retirement conference in London. What is amazing is that whilst much of our industry is stuck in a very product focused approach, selling often what is best for them rather than the client, there is a core of financial planners that are trying to do things better.

Whilst not all of the speakers were for the faint hearted, due to the technicality of their approach, what is amazing is the work that is being done into the science of retirement. Essentially, make sure that people don’t have too much life at the end of their money, and run out when they are no longer able to return to work.

The research that is being done and the technology that is being developed in this area is fantastic. Running models to assess the probability of every client in retirement’s success, and using that to make adjustments to their withdrawal rate to ensure they don’t, is incredibly powerful planning.

The cornerstone of this type of planning is of course Lifetime Cashflow Forecasting. In retirement, it is vital you have the foresight to ensure that whilst you don’t run out, you also do live out your very own dream retirement. The balance of the 2 is most definitely a science, and without careful planning, you risk failing. Ultimately, if you don’t know where you are going, any road will lead you there!

Book

This month’s book recommendation is the brilliant ‘When; The Scientific Secrets of Perfect Timing’ by Dan Pink. Most of Dan Pink’s previous books have been recommended here, and this just might be his best yet. You will notice that we have featured a Learning Lunch on this specific book, so that will give you a feel for it, but I encourage you to read it all the same.

Who would have thought timing was so important to the shape of our lives? School children’s grade’s being determined by the time of day they are tested. Whether someone appearing in court is sentenced or not significantly influenced by the time of day they make their appearance. Which tasks are we better at in the morning than the afternoon, and vice versa?

A brilliant book that will make you think about your day from a totally different perspective.